Yesterday I unlocked my phone, requested a Waymo, waited three minutes for it to arrive, hopped into the driverless vehicle, put on my seatbelt, and was smoothly dropped off 15 minutes later. Just like that. If you aren’t living in SF right now, you might be unaware of how far autonomous driving has progressed. After years of enormous capital inflows, painstaking regulatory processes, an abundance of consumer education and trust building, and a whole lot of investment in tech infrastructure, the last year has seen autonomous vehicles take over our oft-maligned city. Slow at first, then all at once. And I felt a whole lot safer in that Waymo than I do in an Uber. Perhaps because 94% of roadway crashes happen due to human behavior.

What I experienced with Waymo is called Level 4 Automation, the second to last stop on a path towards complete autonomy. At Core, we’re embracing this analogy and applying it to the financial services industry by investing in critical infrastructure that allows for “autonomous finance”- i.e. the idea that technology will automate all financial tasks. The way we borrow, invest, spend, advise, and analyze in financial services will all change significantly over the next decade. Similar to self-driving vehicles, there are stages of automation, regulatory processes, trust building, and tech investment needed to make it happen, but our deep conviction is that autonomous finance will arrive and we want to help lead the way. Recent advancements in AI have reminded the tech world just how it will feel. Slow at first, then all at once.

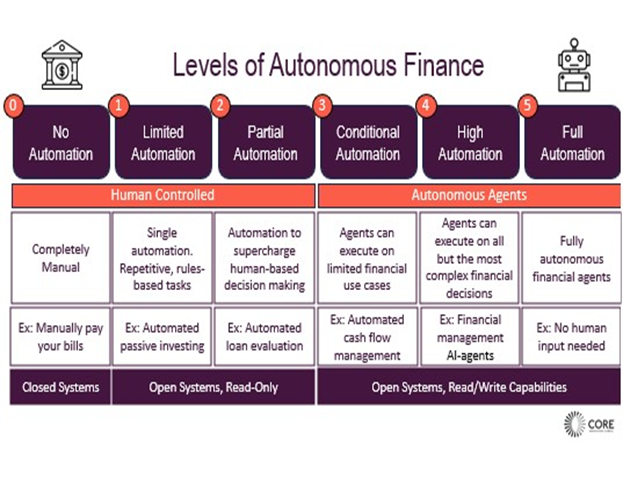

The Stages of Automation

In 2014, the Society of Automotive Engineers (SAE) published the standard definitions for the six levels of automation. The parallels to fintech’s past, present, and future are quite prescient. Finance is following in the tracks of autonomous vehicles, giving us the chance to see what self-driving finance will look like through the lens of autonomous vehicles.

Level 0: No Automation

The human is in complete control. Although there may be systems to help the driver, they are typically just warnings. This automation level requires only very limited sensors. It’s been 30+ years since cars were made with no automation.

Yet, this is how financial services continue to be managed, stubbornly so, today. The consumer handles day-to-day tasks, financial advisors manage money for the affluent, SMB owners manage their back offices to the best of their abilities, insurance agents pitch you insurance you may not need…and so on.

The original fintech darlings were Level 0- no automation, but instead built products to enable users to steer with more confidence. PayPal made accepting online payments simpler and safer, Square united payments acceptance with critical workflows for brick and mortar businesses, now defunct Mint gave you the power to manage your finances outside of a spreadsheet, and Nerdwallet* helped you analyze new financial products. With Level 0 fintechs, we were provided a more comfortable driver’s seat.

Level 1: Driver Assistance

Level 1 automation exhibits a single automated system, such as cruise control, that is applicable to a limited set of circumstances. The driver must still maintain full control. Level 1 requires basic sensors on the car to monitor vehicles in front and behind.

To assist financial drivers, we first needed to make finance more digital and open, which has only happened within the last decade (similar to the explosion in vehicle data in the past decade). In fact, regulators are just starting to codify open finance via CFPB 1033, a proposed rule-making to force financial institutions to make available consumer information. API driven businesses such as Plaid, Atomic*, Drivewealth, and Spinwheel* opened the door to banking, payroll, investing, and credit data, respectively. On top of these platforms, businesses can build simple models to drive low level automation and personalization, and in Level 1 they are doing so to automate repetitive, rules-based tasks. We expect regulation to keep opening the doors to financial data, creating more data pipes on which to build more sophistication.

There are several examples where fintech enables simple cruise control. Betterment and Wealthfront created robo advisory with automated passive investing, letting you pick from a handful of risk tolerances. Digit, acquired by Core portfolio company Oportun*, focused on automating savings based on your cash flows. Tally automated debt reconciliation and made it simpler to pay off debt. Quickbooks used OCR to automate journal entries for SMBs and create user-dictated rules. The driver’s seat now has some basic controls.

Level 2: Partial Driving Automation

In Level 2 the car can control both steering and acceleration/deceleration, but humans still need to actively supervise in the driver’s seat. Hyundai, Kia, and Tesla all have versions of Level 2 automation on the road today. Innovators developed heightened sensors and cameras and designed chips tailored to be able to run more complex algorithms on-vehicle.

Like vehicles, Level 2 autonomous finance represents further sophistication, with humans remaining highly engaged in the driver seat. Automated loan evaluation leads to faster human decisions, AI agents personalize cash flow management recommendations for small businesses and consumers, and AI-enabled RIAs make more informed recommendations, to name a few. In finance, our “heightened sensors” are sophisticated data models and AI/ML algorithms. Businesses such as Prism Data* use ML models to build deeper insights into new data, in this case credit scoring based on a users cash flow. Chalk AI* makes it easy for data teams to compute features in real-time, creating the ability to make far more sophisticated risk decisions. Nilus optimizes business payments and reconciliation. Uprise embeds AI-powered advisory. AI chat bots, such as Bank of America’s Erica, steers through repetitive customer support questions.

Nearly every business is thinking about how it will embrace Level 2 automation to supercharge human “drivers” while minimizing mistakes and avoiding crashes. Much of the near and medium term will be focused on building the infrastructure needed to 10x the productivity of still highly engaged human financial drivers.

Level 3: Conditional Driving Automation

The driver can largely disengage from critical functions in Level 3 automation. The vehicle now has environmental detection, enabling it to make informed decisions such as accelerating past a slow vehicle. Radar and sensors are more sophisticated, requiring the use of lidar and ultrasonic sensors for 360 degree views, continuous monitoring, and redundancy in perceptions. Deep learning models enable these systems to constantly learn and improve. The AI stacks are typically much more sophisticated to include redundancy and fail-safe measures, while handling more data at faster speeds.

Similarly, in finance Level 3 will still include human oversight, but does not require humans to be in complete control. At this point, financial bots will execute on even more informed decisions. Automated loan approvals instead of just evaluations, optimized cash flow management for SMBs not just personalized recommendations, automated investment decisions, optimized tax-allocations…the list of AI agents driving efficiencies goes on and on. To get here, we’ll need more sophisticated data pipelines and “brains” on top of these pipelines, including specialized AI/ML models for specific use cases to add further controls and complement the weaknesses of generalist models (early examples include BloombergGPT for investments or SlopeGPT for b2b payments risk). We’ll need some version of portable digital identities so that a user can retain control of her data, give agency to her AI bots, digitally verify her identity, and enjoy personalized solutions that don’t overstep boundaries (we’re excited about our investment in Self* in this space). We will also advance from utilizing “read-only” APIs where businesses can only read and interpret data to “read/write” APIs where businesses can also alter and update data.

Tangentially, we need continued efficiency and cost reductions to scalably deliver this automation. While there’s no exact science to measure the cost of moving from partial automation to conditional automation, we can directionally look at the jump in cost for large language models GPT2 to GPT3. GPT2 cost $40k to train while GPT3 costs $4m to train. Each model requires many iterations of re-training and fine-tuning, meaning to get GPT3 into production likely required a $100m+ investment. Given that GPT4 apparently has 10x the parameters of GPT3, it will likely again be 10x+ the cost to train. The more sophisticated we get, the more we must rely on exponential efficiency gains (autonomous vehicles face similar obstacles where data storage alone costs upwards of $350k per vehicle).

Perhaps an even greater barrier is the reality that we will need to hand over control to computers, giving our bots limited power of attorney, an idea my partner Arjan has been obsessed about for years. As AI bots become more powerful and complicated, so too does the attendant compliance. Just as regulatory hurdles slowed the pace of autonomous vehicles for the sake of our physical safety, legislative hurdles will appropriately slow the pace of autonomous finance for the sake of our digital and financial safety. Both fintech companies and traditional financial institutions must stay ahead of the curve, earning the trust of users by implementing un-biased AI models only when proper guardrails are in place and adequate explainability is reached. For the foreseeable future, this likely means many use cases where the consumer, advisor, or business will maintain decision making.

Level 4: High Driving Automation

Level 4 automation means the car can now intervene in the case of a system failure, completely driving on its own. The only limitations are certain weather conditions or time of day, enforced by regulation. This requires higher definition maps, real time data processing systems, even more advanced AI algorithms to interpret that data and react to any situation, enhanced failsafes and robust redundancy, and vehicle to vehicle communication mechanisms.

Financial services have a long way to go before reaching Level 4, but the financial agents that we are training today will become even more sophisticated, even more accurate, and even more adaptable than human “agents.” At this level, automated bots will have complete limited power of attorney to make any decision without human intervention – except for a much more limited set of use cases that regulators will define. Agents tailored to engineering, accounting, customer service, and more will power businesses large and small, while consumers will also be armed with agents designed for financial management, negotiations, and every quotidian financial task burdening them today. Similar to vehicles, we need to strive to build immense trust through near-perfect accuracy, robust redundancy measures, and a proper regulatory framework.

Level 5: Full Driving Automation

Level 5 occurs when we’ve reached full autonomy with no practical reason for a human to intervene. Vehicles drive themselves, just as your financial lives will drive themselves.

This world may seem far away, but in technology nothing rings truer than Bill Gates’ legendary observation, “most people overestimate what they can do in one year, and underestimate what they can do in ten.” Slow at first, and then all at once.

Thank you to my partner, Arjan Schütte, who’s ideas and passion for autonomous finance were critical to writing this blog.

*represents Core portfolio companies